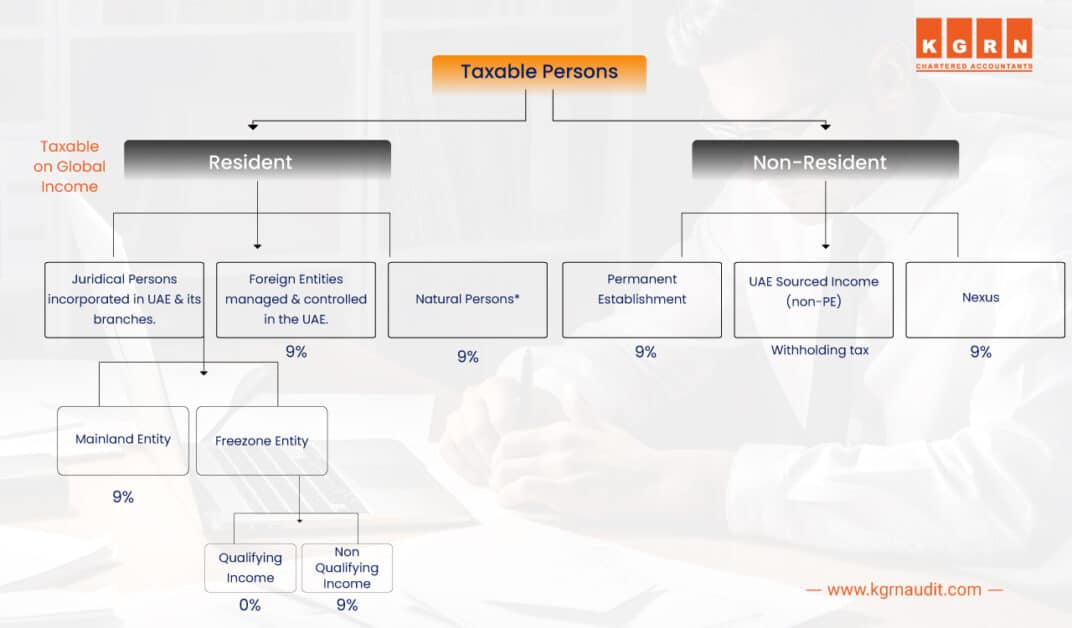

For the purpose of corporate tax, businesses need to understand their tax obligations required to stay compliant with corporate tax law. To achieve this, firstly you need to understand who qualifies as a taxable person. Taxable people are subject to corporate tax and can be classified into two main categories: Residents and Non-Residents.

Article 11 – Taxable Person

A taxable person can be anyone including businesses in UAE, foreign entities, or even individuals under certain conditions. The corporate tax law defines the status to be a resident or a non-resident.

Corporate tax is applicable for a taxable person at the rates specified in the Federal Decree Law No. 47 of 2022.

A taxable person can be a resident person or a non-resident person including natural persons and a branch of a taxable person.

Resident Person

A resident person could be a juridical person or a natural person or a foreign branch incorporated in the UAE

- Resident Juridical Person: A business or an entity that is established under the UAE legislation or under the foreign jurisdiction is known as Juridical Persons under UAE Corporate Tax

- Resident Natural Person: An individual / a human being, conducting a business activity, despite of gender age who may be subject to corporate tax as a taxable person, as per Federal Decree Law No.47 of 2022 is called a natural person.

Non-Resident Person

An entity or a natural person who is not a resident in the UAE are considered as non-residents in the UAE. Non-residents are taxable if they are engaged in a business activity in UAE.

It could be a juridical person operating a business in the foreign country or a natural person who are not engaged in business or business activity in the UAE is regarded as Non-resident Person. This applies to foreign entities and natural persons earning sourced from the UAE.

The non-resident status will be determined by the following factors:

- The business is not established or incorporated in the UAE.

- Not effectively managed or controlled a business in the UAE.

- No physical presence in the UAE for more than 183 days in a calendar year.

There are three main criteria for identifying non-residents such as:

- Permanent Establishment: A non-resident may be considered a permanent establishment, if it maintains a fixed place for a business or conduct a significant business activity within the country.

- State-sourced income: Income derived from the state from business activities or contracts, under the UAE corporate tax law.

- UAE Real Estate Nexus: Income derived from assets in UAE such as land and buildings will fall under the provisions of corporate tax law in UAE.

If a resident person has multiple branches in the UAE, which could be a UAE incorporated companies (including freezone), foreign branches etc, then those branches will be treated as a single tax person, but not as separate entities for corporate tax purposes.

Article 12 – Corporate Tax Base

The income of resident person, which is a juridical person, if earned within the UAE or outside the UAE will be considered as taxable income, in accordance with the provisions of corporate tax law.

The income of a resident person, which is a natural person, is derived from the state or from outside the state insofar it relates to any business or business activity conducted by a natural person upon suggestions of the minister

A Non-Resident Person will be subject to Corporate Tax under the following criteria:

- If the income generated in the state is attributable to the Permanent Establishment of the non-resident person.

- If the income is a state sourced income and not attributable to a permanent establishment of the non-resident person.

- If the Income is derived from the nexus of the Non-Resident Person as provided in a cabinet decision.

Article 13 – State Sourced Income

State-Sourced Income can be broadly categorized into three types, based on the origin of the income and the residency status of the recipient:

- Income Earned by Non-Resident Persons from Resident Persons: Income generated by a Resident Person who is subject to Corporate Tax is considered as state sourced income. Typically, such Resident Persons are allowed to claim deductions for the expenses incurred in generating the taxable income, except if the income is related to a business conducted outside the UAE such as a Foreign Permanent Establishment.

- Income Earned by Non-Resident Persons from Other Non-Resident Persons: This applies when a Non-Resident Person pays income to another Non-Resident Person, if it is generated from a business or activity conducted in the UAE through a Permanent Establishment. Expense deductions is possible under the conditions specified in Article 28 of the Federal Decree Law No.47 of 2022.

- Income from Activities, Assets, Capital, Rights, or Services Within the UAE: The income generated from certain activities, or assets, capital, rights, or services obtained or located within the UAE. This does not consider residential status of the taxable person. Also, the income source is determined based on where the income-generating activity or asset is located or used, not on the contractual relationship between the involved parties.

State Sourced Income refers to income that is generated from activities or assets within the UAE, irrespective of the residential status. This type of income is typically suitable for non-resident persons. If a non-resident person earns income from sources within the UAE, then it must be considered as taxable state-sourced income under corporate tax law.

It is important to understand the classification to determine tax obligations for Non-Resident Persons.

- Income from Selling Goods or Providing Services: The source of income derived from the sale of goods or services will depend on the location where the ownerships of the goods transferred upon sale. This is used to determine for establishing the income source for such transactions. If the ownership of the goods or services transferred within the UAE, then the income is sourced to the UAE. Conversely, if the goods or services sold outside the UAE where the ownership of goods transfers outside the UAE, the income is not considered as state-sourced income.

- Income from Executing Contracts: Any income stemming from contract execution, it can be considered as state-sourced if the obligations for the contract are fulfilled within UAE or the ultimate beneficiary of the contract is located in the UAE.

For instance, if a UAE-based company executes a contract in the UAE, the income is considered state-sourced. Or if the same company executes the contract outside the UAE, the income is sourced outside the UAE.

- Tangible Property Income: Income generated from the sale or utilization of movable or immovable property in the UAE will be considered as state-sourced income. If a company owns and rents a building within the UAE, the income derived from the Income from the sale or utilization of tangible property is also a state source subject to UAE location. This includes revenue generated from property rentals or stakes in such properties, thus categorizing it as State Sourced Income. For example, if a UAE-based company owns and rents out a commercial building in the UAE, the rental income is sourced to the UAE. However, if the same company owns and rents out a similar building outside the UAE, the rental income is sourced outside the UAE.

- Income from Capital Rights Or Disposal Of Shares: Income derived from the sale of shares or rights of the capital of a juridical person, then it is considered as state-sourced income if the juridical person is a resident or incorporated in the UAE. This means if the sale of share where both the seller and the buyer are residents in UAE, then the income is sourced to the UAE. If the seller is a resident and the buyer is a foreign company, then the income is sourced outside the UAE.

- Intellectual or Intangible Property: In case of income derived from intellectual or intangible properties such as trademarks and patents are considered the State sourced income without consideration of the resident status or location of the seller or receiver under corporate tax purposes.

This means that if a UAE-based company provides its patent to a foreign company or an UAE based company, the income will be only sourced to the UAE.

- Income from Interest and Insurance: If a loan is secured by an asset including movable or immovable property, the interest income is considered as state sourced and subject to corporate taxation. If a company in the UAE lends money to a foreign company, the interest income is a state-sourced income.

Article 14 – Permanent Establishment

A Permanent Establishment is the fixed or permanent location in the UAE in which a business is conducted exclusively or partially by a non-resident person.

The following places could be considered as fixed or permanent establishment of business in the UAE:

- A management site where primary business and commercial activities are actively made.

- Offices, Branches, factories, workshops

- Land, buildings, or any other real estate property.

- Structures utilized for extracting renewable or non-renewable resources (e.g., oil wells, gas wells, mines, quarries).

- Any vessels or installations used to extract natural resources.

- A construction site, project or installation, which is active for more than six months. This applies even if the activities are conducted by Related Parties of the Non-Resident Person and are connected.

In some cases, a place will not be treated Permanent Establishment under corporate tax purposes if it is used for:

- Storing, presenting, or delivering goods.

- Holding inventory exclusively to be operated by another party.

- Buying goods or collecting data for the Non-Resident.

- Conducting activities that are preparatory or auxiliary in nature.

The above conditions will not be applicable to the following situations:

- If the auxiliary or preparatory activities go beyond their auxiliary function and collectively contribute to a full business operation

- The same location (or a related location) is used by the Non-Resident or a Related Party for business purposes.

A non-resident person would be considered as a permanent establishment under the following situations:

- If there is a permanent physical presence in UAE to conduct all its activities or business operations.

- If an entity or individual regularly exercises authority in UAE on behalf of the non-resident to conduct a business activity. A person will be deemed to conduct business on behalf of a non-resident person only if they regularly finalize contracts or frequently negotiate contracts finalized by the non-resident person without major changes. It is not applicable for independent agents operating in the UAE, where they conduct their ordinary course of business and are not legally connected with or dependent on the Non-Resident. If they work exclusively for the Non-Resident, they are not considered as independent agent.

- If there is a different form of connection or presence in the UAE as outlined in a Cabinet’s decision upon the Minister’s recommendation.

The Minister may also specify cases similar to the following where a natural person’s presence in UAE will not be eligible for a PE

- Situations that are impermanent and exceptional.

- The employees of the Non-Resident person, where their activities in UAE does not directly contribute to the Non-Resident’s core business process or the Non-Resident does not seem to be generating any UAE-sourced income from such presence.

Article 15 – Investment Manager Exemption

Investment Manager can act on behalf of the non-resident person and can be considered as Independent Agent under the following circumstances:

- The Investment Manager is engaged in a business the offers services such as investment management or brokerage.

- Investment Manager must be subject to the regulatory oversight of the relevant authority in UAE.

- The transactions done during the ordinary course of the business conducted by the Investment Manager.

- The Investment Manager acts in relation to the transactions in an independent capacity.

- The Investment Manager make transactions based on the arm’s length principle with the Non-Resident Person and accepts compensation for provision of such services.

- If a non-resident person uses a local investment manager in UAE, the investment manager will only be considered as acting on behalf of the investment-related activities which is subject to corporate but not as the non-resident person’s representative for other business income or other transactions that are subject to corporate tax.

- Any such other conditions as may be prescribed in a decision issued by the Cabinet at the suggestion of the Minister.

Reference Sources

- 📘 Federal Decree-Law No. 47 of 2022 – UAE Corporate Tax Law

- 🌐 UAE Government Portal – Corporate Tax Overview

- 📊 PwC – Corporate Residence & Permanent Establishment in UAE

- 🏢 TFAB – Permanent Establishment under UAE Corporate Tax

- 📑 KPMG – Guide on Determination of Taxable Income in UAE

Frequently Asked Questions

1. Who is considered a taxable person under the UAE Corporate Tax Law?

A taxable person includes juridical persons (such as companies) and certain natural persons carrying on a business or business activity in the UAE, subject to the provisions of the Corporate Tax Law.

2. What is the Corporate Tax base in the UAE?

The Corporate Tax base is the amount of taxable income on which Corporate Tax is calculated after applying the relevant adjustments, exemptions, and reliefs under the UAE Corporate Tax Law.

3. What is the difference between a resident and a non-resident taxable person?

A resident taxable person is generally a person or entity established or effectively managed in the UAE, while a non-resident taxable person may become subject to Corporate Tax if they have a permanent establishment or sufficient nexus in the UAE.

4. Are individuals considered taxable persons under the UAE Corporate Tax Law?

Individuals may be considered taxable persons if they conduct a business or business activity that falls within the scope of the UAE Corporate Tax Law and meets the applicable conditions.

5. How is taxable income calculated under the UAE Corporate Tax Law?

Taxable income is generally determined based on the accounting profit reported in the financial statements, adjusted for items specified under the Corporate Tax Law.

6. Does the Corporate Tax base include exempt income?

No. Certain types of income may qualify for exemptions or reliefs under the UAE Corporate Tax Law and may not form part of the taxable income, subject to the applicable conditions.

7. What is a permanent establishment under the UAE Corporate Tax Law?

A permanent establishment is a fixed place of business or another form of taxable presence through which a non-resident conducts business in the UAE, making it potentially subject to Corporate Tax.

8. Are Free Zone Persons considered taxable persons?

Yes. Free Zone Persons are generally within the scope of the UAE Corporate Tax regime. However, eligible Qualifying Free Zone Persons may benefit from preferential tax treatment if they meet the prescribed conditions.

9. Why is it important to determine the correct taxable person?

Identifying the correct taxable person ensures proper Corporate Tax registration, accurate tax calculations, timely filing, and compliance with UAE tax regulations.

10. How can businesses determine their Corporate Tax obligations?

Businesses should assess their legal structure, residency status, business activities, and applicable provisions under the UAE Corporate Tax Law. Consulting a qualified tax professional can help ensure accurate compliance.

11. What records should taxable persons maintain?

Taxable persons should maintain proper accounting records, financial statements, invoices, contracts, and supporting documentation as required under the UAE Corporate Tax Law.

12. Can a Corporate Tax consultant help determine the Corporate Tax base?

Yes. A Corporate Tax consultant can help identify taxable income, apply eligible exemptions and reliefs, ensure compliance with the law, and support accurate Corporate Tax filing.