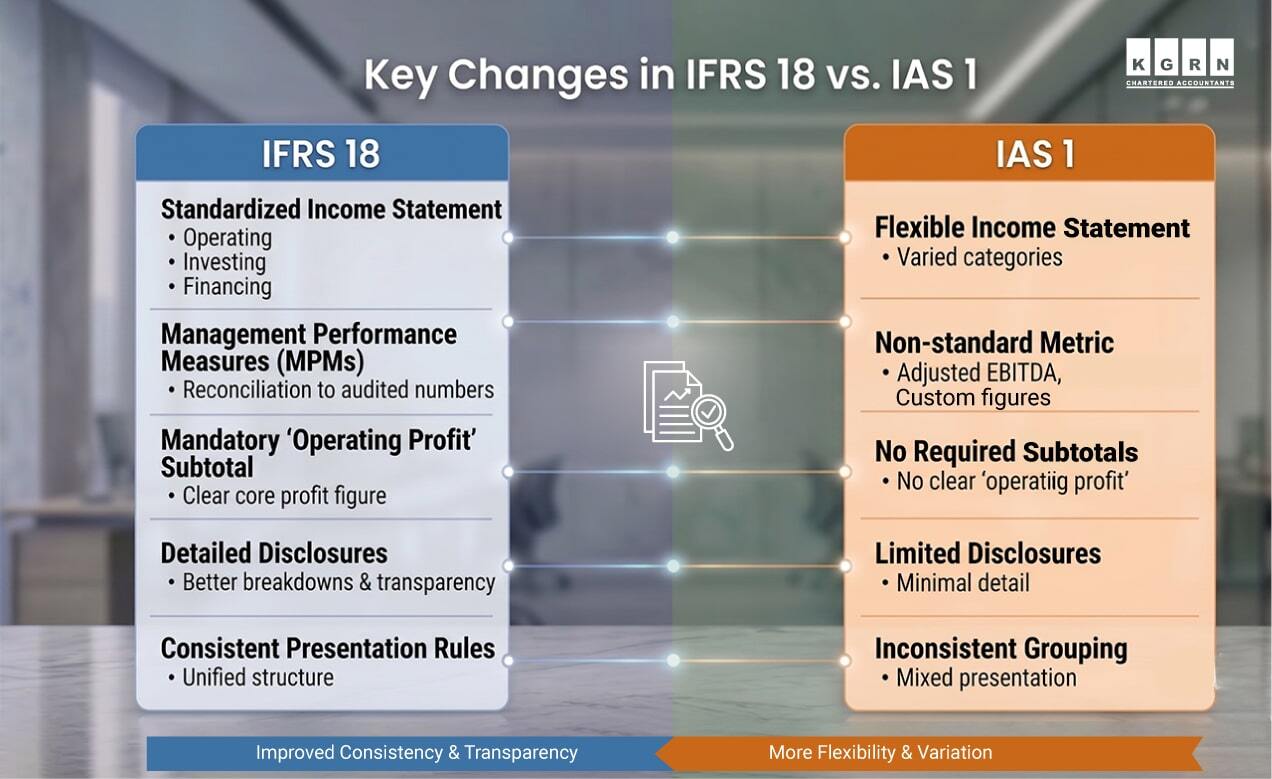

In April 2024, the International Accounting Standards Board (IASB) published a new standard on IFRS 18 “Presentation and Disclosure in Financial Statements.” This brings a major shift in how companies in the UAE submit their financial statements. The new IFRS presentation will replace IAS 1 with the objective of increasing comparability of the financial performance.

IFRS 18 will reshape the structure and clarity of financial reports in accounting, especially in relation to how operating profit or loss is defined.

What is IFRS 18?

IFRS 18 (International Financial Reporting Standards) introduces a clear format for the profit and loss financial statement. This way of reporting helps those who read financial statements understand the information and compare organisations better.

The new standards will apply to reporting periods beginning 1 January 2027, with a requirement to restate comparative information.

Although IFRS 18 replaces IAS 1, many of the existing principles in IAS 1 are retained with limited changes. The new requirements include disclosure requirements for ‘managed-defined performance measures’ (MPM) for transparency.

Key Changes Mandated by IFRS 18

The New Structure in the Presentation of Financial Statement of Profit or Loss

One of the key changes of IFRS 18 is to require all companies to classify items of income and expenses into five categories. The categories include operating, investing, financing, income taxes and discontinued operations.

Even though there are two categories in the play, IFRS 18 introduces three main categories (operating, investing and financing). This provides specific guidance to help preparers in analyzing items to be classified in each respective category.

The new structure helps companies, especially with the main business activities of providing finance to customers and investing in assets. It ensures that their financial statements accurately reflect their operational performance and financial position in accordance with IFRS 18.

Moreover, the objectives of these categories are accompanied by the requirement to present subtotals and totals for ‘operating profit or loss,’ ‘profit or loss before financing and income taxes’ and ‘profit or loss’.

This new standard includes additional instructions related to the aggregation or disaggregation of asset, liability, equity, income, expense, and cash flow items based upon ‘similarities and characteristics’ between them.

Companies must perform these aggregations or disaggregations to create line items in the main financial statements. It ensures the reports present a clear and structured summary for users. In addition, companies must aggregate/disaggregate information in the footnotes of the financial statements based on providing materiality detail while ensuring that materiality detail is clear.

Management Defined Performance Measures (MPMs)

The new standard also introduces management-defined performance measures. An MPM (Alternative Performance Measure) represents a subtotal of revenues and expenditures that companies do not specifically reference in IFRS accounting guidelines or are not required to present or disclose.

When communicating with users outside of public financial statements, MPMs serve as a means for management to communicate their assessment of a specific component of the company’s overall financial results.

Moreover, IFRS 18 requires entities to disclose information about all their MPMs in a single note to the financial statements. Also, it requires disclosure of how the measure is calculated and how it provides useful information to users and a reconciliation to the most comparable subtotal specified by IFRS accounting standards.

Other Limited Changes

IFRS 18 bringing other limited changes to the presentation of financial statements. For instance, IAS 7, statement of cash flow is amended to:

- Starting Point for Reconciliation to Cash Flow from Operating Activities – Operating Profit or Loss and,

- Remove all existing alternative presentations for Interest Paid and Received and Dividends Paid and Received.

Effective Date and Transition

For all annual financial periods beginning on or after 1 January 2027, IFRS 18 will apply retrospectively to determine comparability between financial years. This means the initial application of IFRS 18 will have different effective dates, depending on each jurisdiction’s local regulations.

Companies that choose to apply the standard sooner than 1 January 2027 are required to disclose this in their notes to the financial statements. If the company applies IAS 34 Interim Financial Statements to prepare condensed interim financial statements in its first year of implementation. The company must provide the headings it expects to use when applying IFRS 18.

The headings and subtotals should comply with the standard. Furthermore, companies must provide a reconciliation of each line item presented on the statement of financial performance from the immediately prior two years to the current year and to the cumulative current year.

What’s Different in IFRS 18 from IAS 1

Why UAE Businesses are Directly in Scope

Under Ministerial Decree #84 for 2025, all UAE entities generating total gross revenue exceeding AED 50 million are required to prepare audited financial statements in accordance with IFRS.

These financial statements must also be used for the purpose of corporate tax estimation.

This requirement extends to entities operating within the DIFC and ADGM, where the use of full IFRS accounting policies is already mandatory, as opposed to IFRS for SMEs.

Additionally, companies should note that IFRS 18 will take effect in 2027. They must apply IFRS 18 to financial statements currently under audit to ensure consistency and compliance in upcoming reporting periods.

Why Companies Must Act in 2026, not 2027

Companies adopting IFRS 18 from a December 31 year-end must apply it retrospectively for 2027. They must also restate their financial statements for the 2026 financial year to comply with IFRS 18 requirements.

Companies beginning to prepare for IFRS 18 in 2027 will be subject to severe time pressure when restating their prior periods.

Free Zone QFZP Implications

To keep your Corporate Tax rate at 0%, qualifying Free Zone Persons will need to have their financials audited. As IFRS 18 changes how income and expenses are classified (i.e., operating vs investing vs financing), this could cause a change in one’s ability to identify and present qualifying income.

Companies should also re-evaluate QFZP status assessments under the new income statement structure, especially if they have multiple revenue streams.

Frequently Asked Questions

What is the effective date of IFRS 18?

Beginning January 1, 2027, the International Financial Reporting Standards (IFRS) 18 will take effect. All companies must prepare their annual financial statements in accordance with IFRS 18 and then begin retrospectively preparing relevant 2026 financial statements in accordance with IFRS 18, even if they have a December 31st fiscal year end. Thus companies must start preparing their comparatives in 2026 not 2027.

Does IFRS 18 apply to all UAE companies?

All UAE businesses must create IFRS compliant statements including businesses with taxable incomes over AED 50M; DIFC and ADGM entities; and QFZP companies with Free Zone status must comply with IFRS 18 as of January 2027.

What are the five income/expense categories under IFRS 18?

IFRS 18 requires all income and expenses to be classified into: Operating, Investing, Financing, Income taxes, Discontinued operations. Two new mandatory subtotals are introduced: operating profit and profit before financing and income taxes.

How does IFRS 18 affect UAE corporate tax filings?

The UAE Corporate Tax is assessed based upon the company’s audited financial statements. The implementation of IFRS 18 will cause a change in which income and expenses are categorized and reported by companies. As a result will impact a company’s taxable profit. Companies should ensure that their 2026 comparatives and their 2027 statements are consistent with their Corporate Tax returns when filed in order to avoid audits from the FTA.