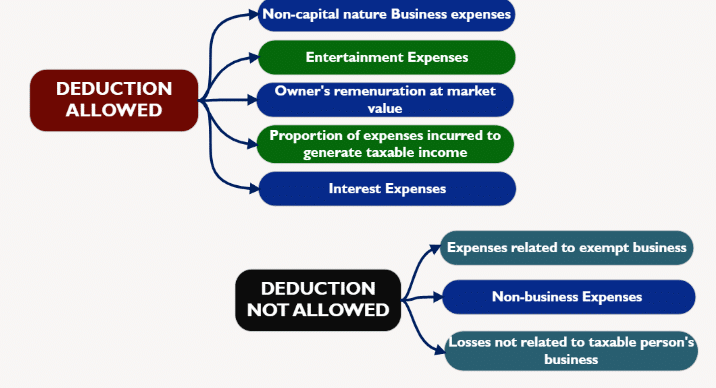

Deductible Expenses–(Article 28)

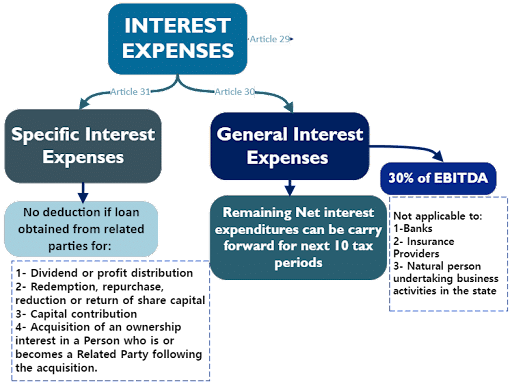

Interest Expenses

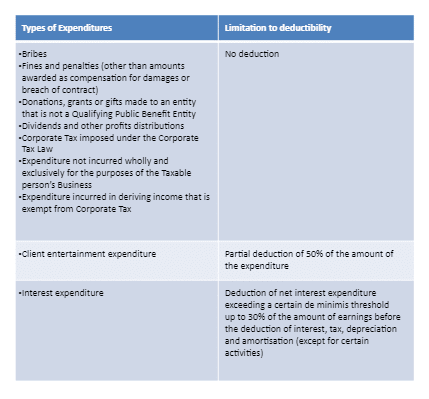

Entertainment Expenditure –(Article 32)

50% of entertainment expenses are deductible. Entertainment include the followings:

a) Meals.

b) Accommodation.

c) Transportation.

d) Admission fees.

e) Facilities and equipment used in connection with such entertainment, amusement or recreation.

Non-Deductible Expenses–(Article 33)

- Donations, grants or gifts to a non-qualifying Public Benefit Entity.

- Fines and penalties

- Bribes or other illicit payments.

- Dividends, profit distributions to the owner of the Taxable Person.

- Amounts withdrawn by taxable natural person or partner in unincorporated partnership.

- Corporate Tax imposed

- Recoverable Input VAT.

- Tax on income imposed on the Taxable Person outside the Stat

Contact us at @ +971 45 570 204 / Email Us : support@kgrnaudit.com, and one of our Corporate tax consultant will provide you with necessary support and consultation.

FAQ

What expenses are deductible?

Contact us at @ +971 45 570 204 / Email Us : support@kgrnaudit.com, and one of our Corporate tax consultants will provide you with necessary support and consultation.

Frequently Asked Questions

1. What are deductible expenses under UAE Corporate Tax?

Deductible expenses are business expenses that are wholly and exclusively incurred for the purpose of generating taxable income and may be deducted when calculating taxable profits, subject to the UAE Corporate Tax Law.

2. What are non-deductible expenses under UAE Corporate Tax?

Non-deductible expenses are costs that cannot be claimed as tax deductions. These may include personal expenses, certain fines and penalties, donations that do not qualify, and other expenses restricted under the UAE Corporate Tax Law.

3. Are employee salaries and wages deductible?

Yes. Employee salaries, wages, bonuses, and other employment-related expenses are generally deductible if they are incurred wholly and exclusively for business purposes.

4. Can businesses deduct entertainment expenses?

Entertainment expenses may be subject to limitations under the UAE Corporate Tax Law. Businesses should review the applicable provisions to determine the deductible amount.

5. Are fines and penalties tax deductible in the UAE?

No. Fines and penalties imposed for violations of laws or regulations are generally considered non-deductible expenses.

6. Is interest expense deductible under UAE Corporate Tax?

Interest expenses may be deductible, but they are subject to specific rules and limitations, including the General Interest Deduction Limitation Rule where applicable.

7. Can depreciation be claimed as a deductible expense?

Depreciation may be deductible if it is recognized in accordance with applicable accounting standards and the provisions of the UAE Corporate Tax Law.

8. Are charitable donations deductible for Corporate Tax purposes?

Only qualifying donations made to approved public benefit entities may be deductible, subject to the applicable Corporate Tax rules.

9. What records should businesses maintain to support deductible expenses?

Businesses should maintain invoices, receipts, contracts, bank statements, payroll records, and other supporting documentation to substantiate deductible expenses.

10. Why is it important to distinguish between deductible and non-deductible expenses?

Correctly classifying expenses helps businesses calculate taxable income accurately, comply with UAE Corporate Tax regulations, and reduce the risk of penalties during tax assessments.

11. Can businesses claim personal expenses as tax deductions?

No. Personal or private expenses that are not related to business activities are generally not deductible under the UAE Corporate Tax Law.

12. How can businesses ensure they claim deductible expenses correctly?

Businesses should maintain proper accounting records, review the latest UAE Corporate Tax guidance, and consult qualified tax professionals to ensure compliance and maximize eligible deductions.

Related Topics

What is the taxable and exempt income for corporate?

Tax Base Analysis of Corporate Tax in UAE

Guide to Registration and Deregistration of Corporate Tax in UAE

Who is exempt from UAE corporate tax?

Taxable Person as per Corporate Tax Law in UAE

Significant CD, MD, and FTA Decisions related to Corporate Tax in UAE