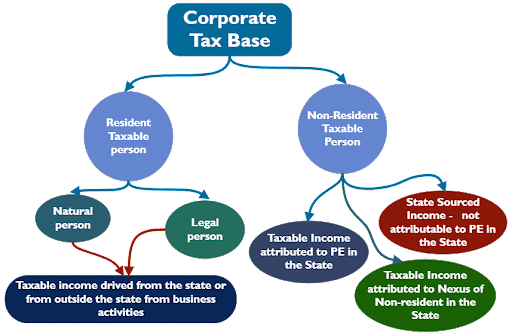

Tax Base –(Article 12)

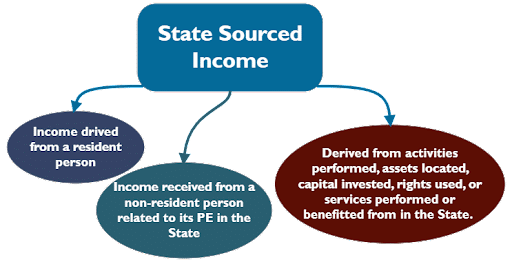

State Sourced Income–(Article 13)

- Income from the sale of goods in the State.

- Income from the provision of services that are rendered or utilised or benefitted from in the State.

- Income from a contract insofar as it has been wholly or partly performed or benefitted from in the State.

- Income from movable or immovable property in the State.

- Income from the disposal of shares or capital of a Resident Person.

- Income from the use or right to use in the State, or the grant of permission to use in the State, any intellectual or intangible property.

- Where it is derived from a Resident Person.

- Where it is derived from a Non-Resident Person and the income received has been paid or accrued in connection with, and attributable to, a Permanent Establishment of that Non-Resident Person in the State.

- Where it is otherwise accrued in or derived from activities performed, assets located, capital invested, rights used, or services performed or benefitted from in the State.

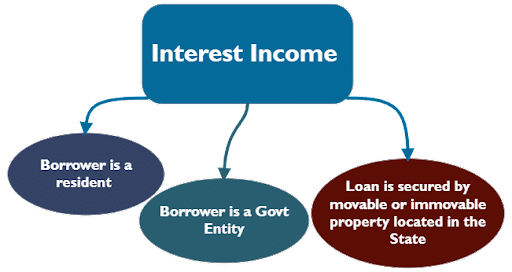

- Interest Income

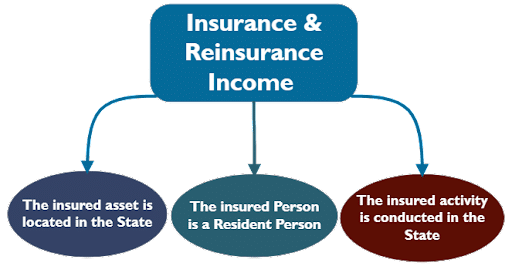

- Insurance and reinsurance premiums

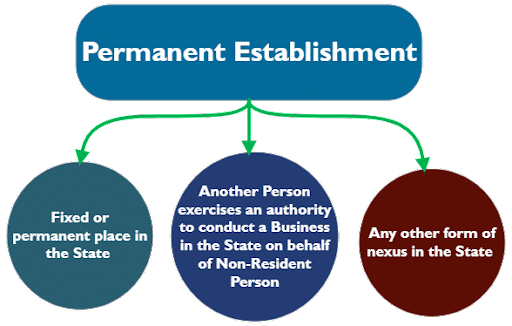

Permanent Establishment–(Article 14)

Fixed or Permanent Place–(Article 14)

- A place of management where management and commercial decisions that are necessary for the conduct of the Business are, in substance, made.

- A branch.

- An office.

- A factory.

- A workshop.

- Land, buildings and other real property.

- An installation or structure for the exploration of renewable or non-renewable natural resources.

- A mine, an oil or gas well, a quarry or any other place of extraction of natural resources, including vessels and structures used for the extraction of such resources.

- A building site, a construction project, or place of assembly or installation, or supervisory activities in connection therewith, but only if such site, project or activities, whether separately or together with other sites, projects or activities, last more than (6) six months, including connected activities that are conducted at the site or project by one or more Related Parties of the Non-Resident Person.

Fixed or Permanent Place–Exceptions (Article 14)

A fixed place or permanent place is not operated by the non-resident person, or its related party or conducting any business activities, such place will not be considered as permanent establishment of the non-resident person if that place is used for:

- Storing, displaying or delivering of goods or merchandise belonging to that Person.

- Keeping a stock of goods or merchandise belonging to that Person for the sole purpose of processing by another Person.

- Purchasing goods or merchandise or collecting information for the Non-Resident Person.

- Conducting any other activity of a preparatory or auxiliary nature for the Non-Resident Person.

Presence of a natural person in the State does not create a Permanent Establishment for a Non-Resident Person in any of the following instances:

a. Where such presence is a consequence of a temporary and exceptional situation.

b. Where the natural person is employed by the Non-Resident Person, and

- The activities being conducted in the State by the natural person are not part of the core income-generating activities of the Non-Resident Person or its Related Parties.

- The Non-Resident Person does not derive State Sourced Income

Investment Manager Exemption–(Article 15)

Investment Manager shall be considered an independent agent when acting on behalf of a Non- Resident Person, if:

- Engaged in the business of providing investment management or brokerage services;

- Subject to the regulatory oversight of the competent authority in the State;

- The transactions (commodities, real property, bonds, shares, derivatives or securities of any other description including foreign currency) are carried out in the ordinary course of Business;

- Acts in relation to the transactions in an independent capacity;

- Carry out the transactions on arm’s length basis

- Receive compensation for the services; and

- Not a representative of non-resident person.

Contact us at @ +971 45 570 204 / Email Us : support@kgrnaudit.com, and one of our Corporate tax consultants will provide you with necessary support and consultation.

FAQ

Who pays corporate tax in UAE?

The starting point for calculating Taxable Income is the Taxable Person’s accounting income (i.e. net profit or loss before tax) as per their financial statements. The Taxable Person will then need to make certain adjustments to determine their Taxable Income for the relevant Tax Period.

For example, adjustments to accounting income may need to be made for income that is exempt from Corporate Tax and for expenditure that is wholly or partially non-deductible for Corporate Tax purposes.

Does accounting profit always equal the corporate tax base?

No, accounting profit does not always equal the corporate tax base. The UAE Corporate Tax Law requires certain tax adjustments to accounting profit before determining the final taxable income. These adjustments ensure that only eligible income and expenses are considered for tax purposes.

Related Topics

- Guide to Registration and Deregistration of Corporate Tax in UAE

- Related Parties & Related Party Transaction Under Corporate Tax

- Who is exempt from UAE corporate tax?

- Taxable Person as per Corporate Tax Law in UAE

- Significant CD, MD, and FTA Decisions related to Corporate Tax in UAE

- Tax Agent Dubai