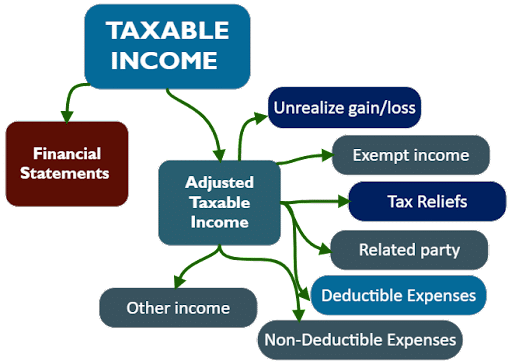

Taxable Income–(Article 20)

Taxable Income– Financial Statements (Article 20)

Taxable Person that prepares financial statements on an accrual basis may elect to take into account gains and losses on a realization basis in relation to:

- all assets and liabilities that are subject to fair value or impairment accounting under the applicable accounting standards; or

- At the end of a Tax Period, all assets and liabilities held on capital account are taken into account, as well as any unrealised gain or loss arising from assets and liabilities held on revenue account.

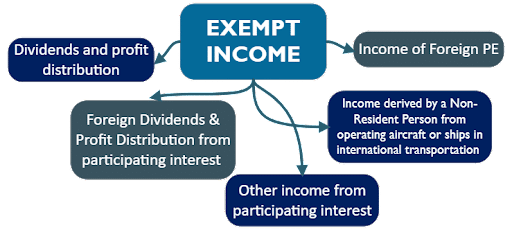

Exempt Income–(Article 22)

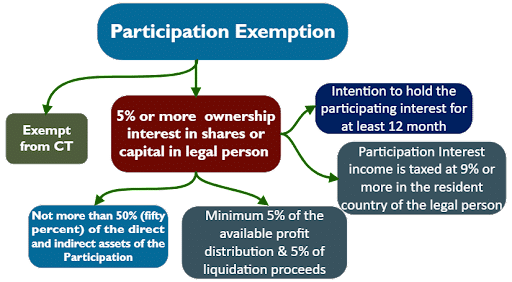

Participation Exemption – Conditions (Article 23)

- The principal objective of the Participation is the acquisition and holding of shares; and

- The income of the Participation derived during the relevant Tax Period substantially consists of income from Participating Interests.

Foreign PE Exemption – (Article 24)

- Taxable Person can make election to exclude the income and associated expenditure

of its foreign PE. - To calculate the income and associated expenditure of a Foreign Permanent

Establishment, a Resident Person and each of its Foreign Permanent Establishments

shall be treated as separate and independent Persons. - Transfer of Assets and liabilities between PE and Resident person must be treated at

market value on the date of transfer. - The exemption is not applicable to the taxable income of foreign Permanent

Establishment.

Non-Resident Person Operating Aircraft or Ships in International Transportation – (Article 25)

If a non-resident individual does the following business activities:

- International transportation of persons, livestock, mail, parcels, commodities, and goods via air or sea.

- Leasing or chartering aircraft or ships used for international travel.

- Leasing of equipment that is critical to the seaworthiness of ships or the airworthiness of planes used in international travel.

The exemption is only applicable if the non-resident person is also exempt for the corporate tax on similar business in the country of residence.

Contact us at @ +971 45 570 204 / Email Us : support@kgrnaudit.com, and one of our Corporate tax consultants will provide you with necessary support and consultation.

Related Topics

Guide to Registration and Deregistration of Corporate Tax in UAE

Who is exempt from UAE corporate tax?

Taxable Person as per Corporate Tax Law in UAE

Overview of Related Parties & Related Party Transaction Under Corporate Tax

Significant CD, MD, and FTA Decisions related to Corporate Tax in UAE

FAQs

What is the UAE’s corporation tax rate?

The UAE Corporate Tax rate is 0% on taxable income up to AED 375,000, and 9% on taxable income above that amount. This arrangement is intended to promote small enterprises while imposing standard taxation on larger profits.

Are small firms exempt from UAE corporate taxes?

If a small business’s revenue falls below the Federal Tax Authority’s threshold, it may be eligible for Small Business Relief. This relief permits eligible businesses to be considered as if they had no taxable revenue for a set period of time, lowering their corporate tax burden.

Is personal income liable to UAE Corporate Tax?

No, personal income, such as salary, investment income, or personal real estate income, is normally exempt from UAE Corporate Tax. The tax mostly relates to corporate and commercial activity conducted in the UAE.

Are corporations required to keep accounting records for corporate taxes?

Yes, businesses subject to UAE Corporate Tax must keep proper accounting records and financial statements in order to compute taxable income accurately. These records must be retained for regulatory purposes and potential audits by authorities.