Article 4,5,6,7,8,9, & 10 Of Federal Decree Law No. 47 of 2022

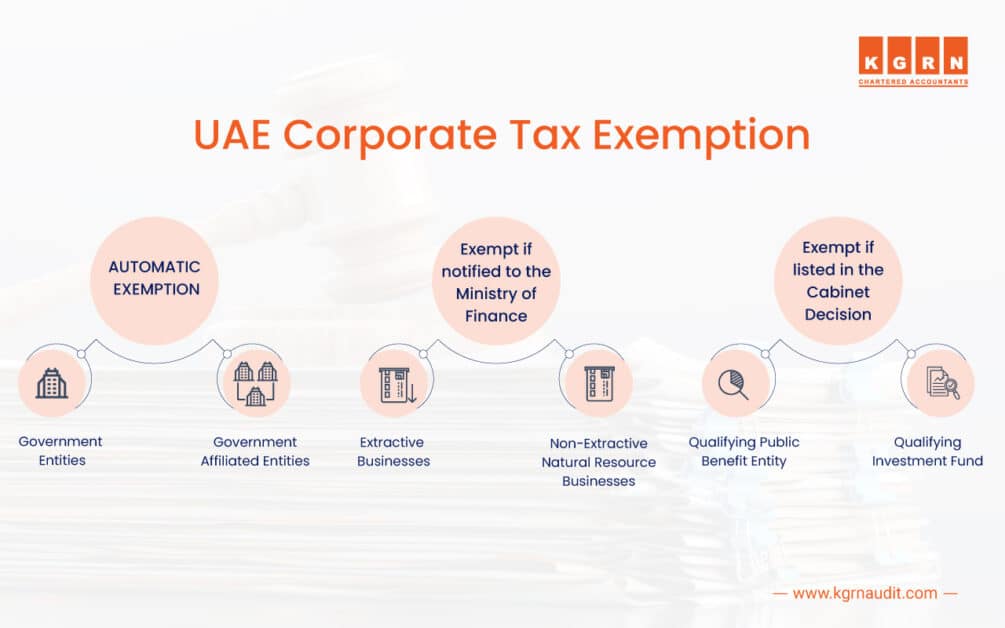

Let us explore chapter three of the UAE Corporate Tax Law which covers exempt categories such as government entity, extractive businesses, non-extractive natural resource business, qualifying public benefit fund entity, and qualifying investment fund.

The corporate tax in UAE has introduced Federal Decree law No. 47 of 2022, in 2022 and became effective for financial years starting on or after 1 June 2023. The Federal Tax Authority (FTA) has set out several thresholds such as

For Businesses Excluding Qualifying Free Zones and Multinational Corporation

The Corporate Tax Rate is 9% for revenue above AED 375,000 and 0% for below the threshold.

For Multinational Corporations

The multinational enterprises with a consolidated revenue of above EUR 750 million, for at least two of the four financial years preceding the current tax year will be subject to Domestic Minimum Top-up Tax (DMTT) at the rate of 15%.

Article 4 – Exempt Person

As per the Federal Decree law No. 47 of 2022, the following Persons are eligible for exemption from the corporate tax:

- Government Entities

If an entity belongs to a federal or Emirate-level government authority, then it naturally exempted from the corporate tax. This includes federal departments, ministries, and other governmental institutions etc, and these must not be involved in commercial undertakings outside the scope government responsibilities.

- Government Affiliated Entities

Entities that are owned by the government are also eligible to be exempt under certain conditions. The exemption is applicable only for certain activities that are mentioned in the Cabinet Decision. If an entity receives income outside those activities, that is considered as taxable income.

- Extractive Businesses

Entities that conduct activities involving extracting natural resources – like oil and gas will be exempt from corporate tax, only if they:

- Are under the scope of Emirate-level taxation

- Have a valid trade license issued by the local government.

This helps such businesses to avoid double taxation in multiple jurisdictions across federal and Emirate levels.

- Non-Extractive Natural Resource Businesses

If the business activity of an entity involves natural resources (but doesn’t include water extraction), such as solar energy, air, and wind and if it is taxed under any other Emirate regime, it may also be eligible for exemption. It is crucial that the entity must adhere to licensing and reporting regulations of the region, as they can be the determining factor to qualify for exemption.

- Qualifying Public Benefit Entity

Qualifying public benefit entities consist of various organizations that conduct charitable activities including charities, non-profits, foundations, and associations to serve for the purpose of social, religious, cultural, or education. These entities are required to:

- Apply to the FTA

- Be listed as public benefit fund entity in a Cabinet Decision

- Strictly operate within their scope of operations

Note: If you are running a charitable entity or non-profit organization, that does not mean you are automatically exempt from corporate taxation, it is important to obtain official recognition from the authority and maintain proper records.

- Qualifying Investment Fund

Investment funds that satisfy the following conditions may qualify for exempt if they:

- Are subject to regulatory oversight of competent authority

- Are not primarily engaged in any commercial activity

- Satisfy additional conditions set by the tax authority.

Each fund should be assessed individually, so get expert guidance to ensure you are a qualified investment fund for exemptions. As an FTA-approved corporate tax agent, KGRN Chartered Accountants help businesses to understand the intricacies of the corporate tax law and navigate the processes through our comprehensive corporate tax services in UAE

- Public pension or social security fund, or private pension or social security fund

Only pension and security funds (public and private) approved by the authority will consider as exempt persons under corporate tax law only if they satisfy the specified conditions for their category. It is advised that any organization managing such funds needs to go through relevant cabinet and ministerial decisions to make sure they meet the qualifying criteria and maintain their status as Qualifying Investment Fund.

- Juridical Person

If a juridical person incorporated in UAE that is wholly owned and controlled by an Exempt Person will be exempt under corporate tax law, if it conducts any of the following:

- Undertakes partial or whole of the Exempt Person’ activity.

- Engaged in activities like investing funds or holding assets that benefit the Exempt Person.

- Only conduct activities that are secondary to the activities carried out by an Exempt Person

- Any other Person may be determined as exempt person if mentioned in the cabinet decisions by the authority.

Article 5 – Government Entities

Article 5 of Federal Decree Law explains why government entities are exempt from corporate tax and their eligibility criteria for exemption.

Government entities are exempted from Corporate Tax and the provisions of the Corporate Tax Law will not be applicable to them. The government entities will fall under the scope of corporate tax if they conduct a business or business activity through the license issued by the licensing authority. Then such activity would be treated as an independent business, and the government entity should maintain the financial statements separately for the business.

Since income derived from such business or business activities is taxable and it must be independently calculated for each tax period. Moreover, any transactions between the licensed businesses of the government entity with its entities that perform other exempt activities would be considered as Related Party transactions and will fall under the scope of related parties and control law.

A government entity can apply to the authority to be treated as a single taxable person for the purpose of corporate tax, for all its business or business activities when certain conditions are met.

| Government Entity | |

| Non-Licensed Activities | Licensed Activities |

| Exempt From Corporate Tax | Income Is Taxable Under Corporate Tax Law |

| Need Not Maintain Records | Should Maintain Financial Statements for Each Tax Period |

| Transactions With Licensed Activities Are Considered ‘Related Party transactions’ | Transactions With Both Licensed & Non-Licensed Activities Are Considered ‘Related Party transactions’ |

Article 6 – Government-Affiliated Entities

Here are the conditions and criteria to be exempt from corporate tax for the government-controlled entities:

- By default, the government-controlled entities would be exempted from the Corporate Tax and the factors of the Decree Law would not be applied

- These entities only be affected by the provisions of the corporate tax law, if they conduct a business or business activity that is not their mandated activity. Then such activity that is non-obligatory will be treated as an independent business under corporate tax regulations.

- The affiliated entities conducting this activity should separately maintain financial statements of the business activity apart from the mandated activity.

- For every tax period, it is required for affiliated entities to calculate the Taxable Income independently for business activity that is not their mandatory activity.

- Transactions of the government-affiliated entities made for such non-obligatory tasks with its other activities would be considered Related Party transactions, under the provisions of Related Parties and Control Law.

Article 7 – Extractive Business

- A Person running an Extractive Business will be exempt from corporate tax, if the person:

- Is directly or indirectly interested in a right, or license issued by the local Government to undertake the extractive business.

- Is subject to tax under the Emirate legislation based on the exemptions criteria if the local government imposes the tax.

- A person notifies the Ministry in the manner agreed by the local government

- If a person runs an Extractive Business as well as another business activity will also be eligible for exemption under the following conditions:

- Income generated from the Extractive Business will be subject to tax as per the applicable legislation of the Emirate.

- Income derived from other businesses of the person will be affected by the provisions of the Corporate Tax Law, unless it is a Non-Extractive Natural Resource Business.

- A person should not be considered to inherit income from any business where it is ancillary or supportive to the Extractive Business. Moreover, the revenue generated from such business during the Tax Period does not exceed 5% of the total revenue of the person in the same tax period.

- To calculate the taxable income of the other businesses of a person, the following factors need to be considered.

- The other businesses to be treated as independent business, and the financial statements must be maintained separately from the Extractive Business

- The common expenditure of both Extractive Business and other Business of a person can be apportioned in proportion to the revenue generated during the tax period, unless such expenses is accounted in various proportions for calculating taxable income under the relevant Emirate regulations, where the expenditure is apportioned in the latter proportion.

- The person can calculate taxable income for their other business independently for each tax year, as per the provisions of the Corporate Tax Law

- A person will be subject to corporate tax under the regulations if the Local Government imposes a tax on income or profit, such as revenue or royalty tax, or any form of tax, regarding the Extractive Business of that person.

The above-mentioned exemptions will not be applicable for contractors, producers, subcontractors, or any person who is a part of the Extract Business.

Article 8 – Non-Extractive Natural Resource Business

- A non-extractive business of a person can be exempted from the corporate tax under the following conditions:

- Is directly or indirectly interested in a right, concession or license issued by the local Government to undertake the Non-extractive Natural Resource Business.

- The income derived from the Non-Extractive Natural Resource Business of a person is inherited completely from those who own a business or a business activity

- Is subject to tax under the Emirate legislation based on the exemptions criteria if the local government imposes the tax.

- A person notifies the Ministry in the manner agreed by the local government.

- The following conditions are applicable under corporate tax law if a person generates income an Non-Extractive Business as well as another business activity:

- Income generated by the Non-Extractive Business will be subject to tax as per the applicable legislation of the Emirate.

- The income derived from other businesses of the person will be affected by the provisions of the Corporate Tax Law, unless the business meets the conditions to be exempted from the corporate tax law.

- A person should not be considered to inherit income from any business where it is ancillary or supportive of Non-Extractive Business. Moreover, the revenue generated from such business during the Tax Period does not exceed 5% of the total revenue of the person in the same tax period.

- In order to calculate the taxable income of the other businesses of a person, the following factors need to be considered.

- The other businesses to be treated as independent business, and the financial statements must be maintained separately from the Extractive Business

- The common expenditure of both Non-Extractive Business and other Business of a person can be apportioned in proportion to the revenue generated during the tax period, unless such expenses is accounted in various proportions for calculating taxable income under the relevant Emirate regulations, where the expenditure is apportioned in the latter proportion.

- The person can calculate taxable income for their other business independently for each tax year, as per the provisions of the Corporate Tax Law

- If the Local Government imposes a tax on income or profit, such as revenue or royalty tax, or any form of tax, the person will be subject to corporate tax under the regulations, regarding the Non-Extractive Business of that person.

Contractors, producers, subcontractors, or any person those who are a part of Non-Extractive Business will not be applicable for the above-mentioned exemptions.

Article 9 – Qualifying Public Benefit Fund Entity

The following are the conditions to be exempted as qualifying public benefit funds under corporate tax regulations.

- If the entity is established or deployed for any of the following purposes:

- For religious, charitable, athletic, scientific, healthcare, educational, animal protection, athletic, humanitarian, and other similar reasons.

- As a chamber of commerce, professional unit, or similar unit managed wholly for the purpose of social welfare or public benefit.

- It does not conduct any business or business activity, exempt if the activity is related to or aimed to fulfil the core purpose of the establishment of the entity.

- The income should not be payable to any member, shareholder, trustee, settlor or founder of the entity, if so, it is not considered a Qualifying Public Benefit Entity, Government Entity or a Government Controlled Entity.

- The criteria become effective from the beginning of the tax period, when the public benefit fund entity is listed in the cabinet decision which will be declared based on the suggestions of the minister.

- The authority might request for any records or relevant information from the qualifying public benefit fund entity, which must be submitted within the specified timeline, to monitor the continue compliance with the regulatory requirements.

Article 10 – Qualifying Investment Fund

Qualifying investment funds will be exempted from corporate tax under the conditions below:

- The investment fund or the manager of the investment fund is under the supervision of the relevant authority in the state or a foreign competent authority.

- Investment fund interests are traded on a Recognized Stock Exchange or marketed and made available to the investors

- The establishment of the investment fund should not be to avoid corporate tax

- The authority might request for any relevant information or records from the qualifying investment fund that needs to be submitted within the timeline, in order to monitor the continue compliance with the regulatory requirements of the corporate tax law.

Why Are Certain Entities Exempted from Corporate Tax?

In an effort to boost economic growth and provide a dynamic environment for businesses and investors, the UAE government has provided exemptions in taxation.

The reason behind exempting certain entities from UAE corporate tax is connected to various factors such as:

To Avoid Double Taxation:

If a company operates in multiple locations and needs to be prevented from being taxed in multiple jurisdictions, exemptions are made in such cases. For example, a foreign company could be taxed in their native jurisdiction and will be exempted from UAE corporate tax.

Facilitate Strategic Industries:

By introducing exemptions for freezones, and qualifying public benefit fund entities, the UAE aims to be a dynamic business hub. This ultimately attracts investment and fosters growth in the key economic sectors such as trade and finance.

Support Social Welfare and Public Benefit:

To demonstrate its care for the community, the UAE government supports certain activities that benefit the community or promote social welfare, by offering tax exemptions. This includes public service entities such as charities, religious organizations, and healthcare providers etc.

Encourage Small Businesses:

Small businesses are also exempt from corporate tax if their revenue is below AED 3.75 million. This reduces the financial burden of the companies and also enables them to invest their profits and work towards the growth of the company as well as the economy.

KGRN Chartered Accountants – FTA-Approved Corporate Tax Agent

We provide end-to-end guidance for businesses, to navigate every aspect of the corporate tax. Our corporate tax consultants will take care of the tax procedures, allowing you to stay focused on your core operations, reducing the burden of complying with corporate tax obligations. We will operate as your corporate tax compliance partner, ensuring your tax processes are handled well so you can lead with confidence, clarity, and peace of mind. Reach out to our tax consultants today!

Related posts:

Chapter Four – Taxable Person & Corporate Tax Base Under UAE Corporate Tax Law

Chapter Four – Taxable Person & Corporate Tax Base Under UAE Corporate Tax Law  MoF New Decision – Unincorporated Partnerships

MoF New Decision – Unincorporated Partnerships  Corporate Tax Accounting Standards in UAE: A Guide For Businesses

Corporate Tax Accounting Standards in UAE: A Guide For Businesses  Complete Guide to General Interest Deduction Limitation Rule in UAE Corporate Tax

Complete Guide to General Interest Deduction Limitation Rule in UAE Corporate Tax  Caculation of Corporate Tax liability & Reliefs

Caculation of Corporate Tax liability & Reliefs