Caculating Corporate Tax liability

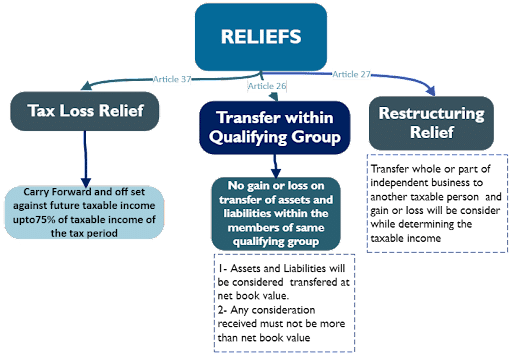

Corporate Tax Reliefs

Transfer of Tax Loss–(Article 38)

Tax loss can be offset against taxable income of another person if:

- Both Taxable Persons are juridical persons.

- Both Taxable Persons are Resident Persons.

- From the beginning of the relevant tax period, either Taxable Person holds a direct or indirect ownership interest in the other of at least 75%.

- None of the Persons are an Exempt Person.

- None of the Persons are a Qualifying Free Zone Person.

- The Financial Year of each of the Taxable Persons ends on the same date.

- Both Taxable Persons use the same accounting rules to generate their financial accounts.

Tax Return

- A Taxable Person is required to file a Tax Return no later than (9) nine months after the end of the applicable Tax Period.

- The tax period is the taxable person’s financial year (Gregorian calendar year), or the (12) twelve-month period during which the Taxable Person files financial statements.

To complete a tax return for CT folloing information will be included:

a) The Tax Period to which the Tax Return relates.

b) The name, address and Tax Registration Number of the Taxable Person.

c) The date of submission of the Tax Return.

d) The accounting basis used in the financial statements.

e) The Taxable Income for the Tax Period.

f) The amount of Tax Loss relief claimed.

g) The amount of Tax Loss transferred

h) The available tax credits claimed

i) The Corporate Tax Payable for the Tax Period.

Tax Settlement–(Article 44)

The Corporate Tax due under this Decree-Law is settled in the following order:

- First, by using the Taxable Person’s available Withholding Tax Credit;

- Foreign Tax Credit

- Relief Options, The outstanding tax liability must be paid within 9 months of the end of the applicable tax period.

Tax Refund–(Article 49)

In the following conditions, a Taxable Person may apply to the Authority for a Corporate income tax refund in accordance with the requirements of the Tax Procedures Law:

Transitional Rules–(Article 61)

- A Taxable Person’s opening balance sheet for UAE Corporate Tax purposes shall be the closing balance sheet prepared for financial reporting purposes under accounting standards applied in the State on the last day of the Financial Year that ends immediately before their first Tax Period commences, subject to any conditions or adjustments that may be prescribed by the Minister.

- The opening balance sheet shall be prepared taking into consideration the arm’s length principle

Categories of Taxable Persons Required to Prepare and Maintain Audited Financial Statements –MD-82 2023

The following Taxable Persons must compile and maintain audited financial statements for the purposes of Clause 2 of Article 54 of the Corporate Tax Law:

- A Taxable Person whose Revenue exceeds AED 50,000,000 (fifty million UAE dirhams) during the applicable Tax Period.

- A Qualifying Free Zone Person.

Contact us at @ +971 45 570 204 / Email Us : support@kgrnaudit.com, and one of our Corporate tax consultant will provide you with necessary support and consultation.

FAQ

Who is subject to Corporate Tax?

Broadly, Corporate Tax applies to the following “Taxable Persons”:

- UAE companies and other juridical persons that are incorporated or effectively managed and controlled in the UAE;

- Natural persons (individuals) who conduct a Business or Business Activity in the UAE as specified in a Cabinet Decision to be issued in due

course; and - Non-resident legal persons (foreign legal organisations) have a Permanent Establishment in the UAE (as defined in [Section 8]). Legal entities incorporated in a UAE Free Zone are also subject to Corporate Tax as “Taxable Persons” and must follow the conditions outlined in the Corporate Tax Law UAE. A Free Zone Person who meets the qualifications to be considered a Qualifying Free Zone Person, on the other hand, can benefit from a Corporate Tax rate of 0% on their Qualifying Income (the conditions are detailed in [Section 14]). Non-residents who do not have a Permanent Establishment in the UAE or who generate income from the UAE that is not related to their Permanent Establishment may be liable to Withholding Tax (at 0%). Withholding tax is a type of Corporate Tax that is collected at the source by the payer on behalf of the income receiver. Many tax systems have withholding taxes, which typically apply to the cross-border payment of dividends, interest, royalties, and other types of income.

Who should Register, file and pay Corporate Tax?

All Taxable Persons (even those in Free Zones) must register for corporate income tax, UAE and get a Corporate Tax Registration Number. Certain Exempt Persons may also be required to do Corporate Tax registration by the Federal Tax Authority. Taxable Persons must file a Corporate Tax return for each Tax Period within 9 months of the end of the applicable period. exactly the same

Contact us at @ +971 45 570 204 / Email Us : support@kgrnaudit.com, and one of our Corporate tax consultant will provide you with necessary support and consultation.

Related Topics

Guide to Registration and Deregistration of Corporate Tax in UAE

Who is exempt from UAE corporate tax?

Taxable Person as per Corporate Tax Law in UAE

What is the taxable and exempt income for corporate?

Tax Base Analysis of Corporate Tax in UAE

Overview of Related Parties & Related Party Transaction Under Corporate Tax

Significant CD, MD, and FTA Decisions related to Corporate Tax in UAE