Business valuation in Dubai has become a recurring compliance function. The way you value your assets now directly affects how much corporate tax you pay and whether the FTA accepts your numbers.

But business valuation is no longer only for mergers and acquisitions or capital raising. Corporate tax means every revaluation of your property and every related party transaction, and every corporate tax return on your books, has a valuation implication.

Three recent regulatory framework changes by the Federal Tax Authority have additionally elevated the importance of business valuation in Dubai: CTP009 alters the computation of excluded gains under the transitional provision for real estate developers; Ministerial Decision No. 173 in 2015 clarifies the impact of the depreciation of investment assets on taxable income. Now, the UAE transfer pricing rules require arm’s length pricing for all business transactions entered into by related parties to be documented and recorded.

What’s new in the business valuation laws, why it’s important, and what your Finance team needs to know about it before the next return.

Key Regulatory Changes of Business Valuation in Dubai 2026

-

Clarification introduced by CTP009 in the applications of Ministerial Decision No. 120 of 2023

The FTA’s clarification focuses on how real estate developers should apply the valuation method under the Transitional Rules in Ministerial Decision No. 120 of 2023 when disposing of Qualifying Immovable Property (QIP).

Key Clarification:

- Project-level application: Entities can apply the transitional rules project by project, instead of having to apply them across the whole entity/unit.

- Four-step calculation: Step 1 — Excluded gain: calculate this as the difference between (i) the market value at the start of the first Tax Period and (ii) the higher of the property’s original cost or its net book value. Step 2 – Allocate excluded gain to Tax Periods in line with revenue recognition under IFRS 15. Step 3 – Allocate accounting profits for the QIP component; no adjustment is allowed in any Tax Period if this leads to an accounting loss. Step 4 – Deduct the excluded gain to eliminate accounting profits (to the extent of the profits).

- Per-QIP (Qualifying Immovable Property) election: The election must be made separately for each QIP.

- Authorised valuers mandated: Company valuation must be determined by the relevant government authority in each Emirate, the DLD in Dubai or the DMA in Abu Dhabi. On the other hand, it can be handled by accredited third-party valuers authorised by those authorities. Moreover, the market value must relate only to the QIP itself. If the company valuation covers property beyond the QIP scope, it will not be accepted unless reasonable adjustments are made to isolate the QIP value.

What this means for real estate CFOs

The Transitional Rules are designed to protect developers from having to pay tax on gains they made before the introduction of the corporate tax registration. If you owned a development project prior to the start of your first Tax Period, you may be entitled to exclude some of your gain from income but it is not a free relief, not a blanket relief, and not a relief you can undo.

The per-QIP election is the most overlooked aspect of the FY 2024 returns. If you elected to treat the election as a blanket decision for all properties rather than a formal election for each QIP or unit, your return may not match CTP009. It is a gap that the FTA can exploit to disallow the transitional relief altogether for the affected QIPs.

Ministerial Decision No. 173 of 2025 on Depreciation Adjustments for Investment Properties Held at Fair Value

The UAE Ministry of Finance issues Ministerial Decision No. 173 of 2025 on 23 June 2025. This decision, effective for tax periods starting on 1 January 2025, closes a gap that has existed since the introduction of CT. Businesses accounting for investment property under the fair value model (IAS 40) previously could not claim depreciation for tax purposes.

Key Points from the Decision:

- Who qualifies: Taxable persons who prepare financial statements on an accrual basis and have elected or simultaneously elect the realization basis for gains and losses under Article 20(3) of the UAE corporate tax law. The election applies to all qualifying investment properties held at fair value. You cannot apply it selectively to individual properties.

- Depreciation rate: The annual deduction is the lower of 4% of the original cost or the tax-written-down value at the start of the relevant tax period. The deduction is prorated for periods shorter or longer than 12 months.

- Realization basis: The Ministerial Decision No. 173 of 2025 provides a one-time exception allowing a taxable person to elect the realization basis and the depreciation election within the same tax return, even if the standard deadline under MD 134 of 2023 was previously missed. This window does not carry forward.

- Deferred tax: The reduction in income tax expense, due to depreciation, results in a temporary difference. UAE business owners must report a deferred tax liability on their financial statements, which is an important accounting impact and should be tested before the decision is made.

Transfer Pricing is Now a Valuation Challenge, Not Just a Tax One

The UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022) applies the Arm’s Length Principle to related-party transactions in line with the OECD Transfer Pricing Guidelines. Ministerial Decision No. 97 of 2023 sets out the transfer pricing documentation requirements issued by the Ministry of Finance.

Key Points from transfer pricing:

- Board Coverage: The Arm’s Length Principle applies to any UAE taxable person that enters into transactions with related parties or connected persons.It applies no matter how small or large the transaction is, whether the entity is in a Free Zone, or what corporate tax rate applies.

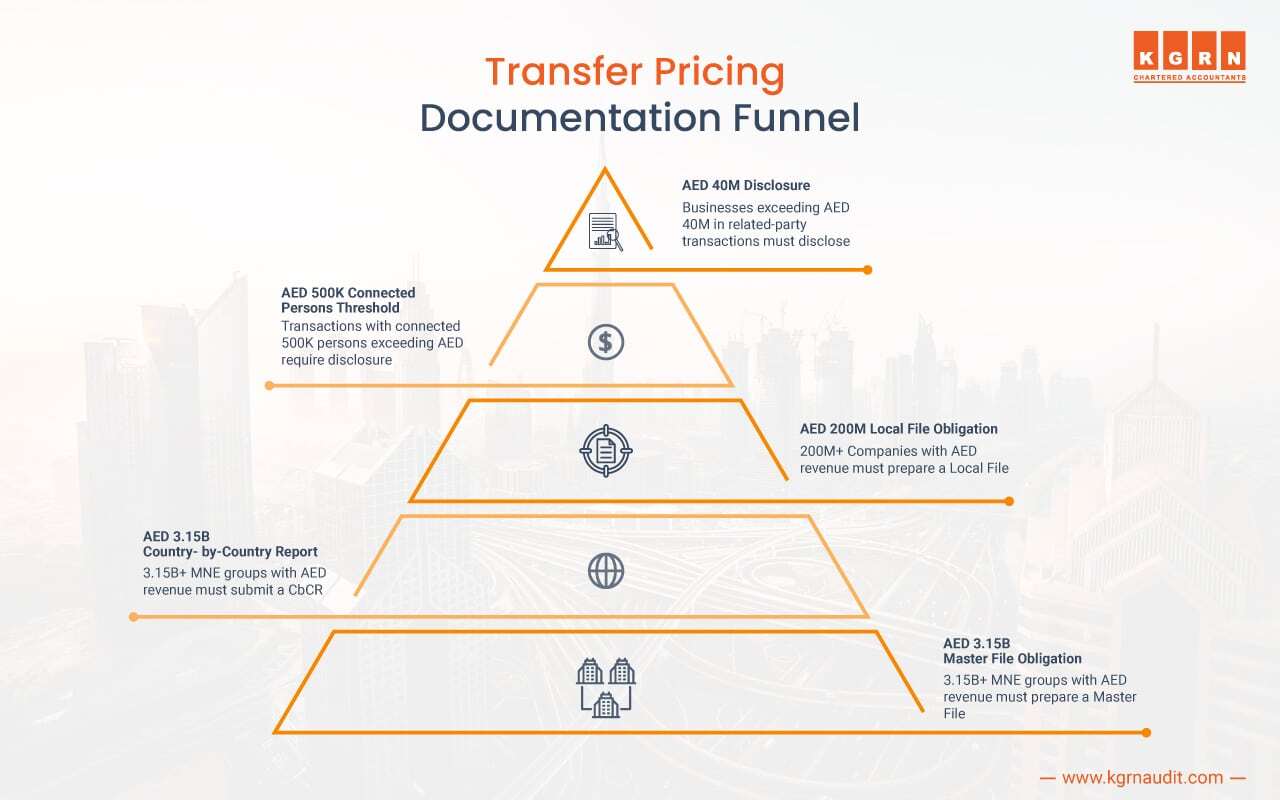

- AED 40 aggregate disclosure: UAE businesses whose total related-party transactions exceed AED 40M must complete the Related Party Disclosure Schedule in their CT return. Individual transaction categories exceeding AED 4M must be separately disclosed.

- AED 500K connected persons threshold: Transactions with connected persons must be individually disclosed where benefits to that person AED 500,000

- Local File obligation: AED 200M: AED 200M: Companies with UAE revenue of AED 200M or greater must prepare a Local File. Note: a UAE entity which meets this threshold but whose entire ownership structure is UAE-resident has no Master File obligation, only a Local File obligation.

- Master File obligation: Businesses with a taxable person who is part of a Multinational Enterprise (MNE) group with consolidated group revenue of AED 3.15 billion or more must prepare a Master File. A UAE-only conglomerate (where all entities are resident in the UAE) is obliged to prepare a Local File, but not a Master File, if consolidated group revenue is less than AED 3.15 billion.

- Country-by-Country Report: MNE groups with worldwide consolidated revenue of AED 3.15 billion or more must submit a Country-by-Country Report under Cabinet Resolution No. 44 of 2020. The UAE ultimate parent entity must notify the Ministry of Finance by the last day of the group’s financial year, and file the CbCR within 12 months after the financial year-end.

- Documentation to be prepared contemporaneously: The Local File, Master File and benchmarking study must be prepared at the time of the transactions, not at the time of the FTA request. The taxpayer bears the burden of proof.

- 30 days to produce: Master File and Local File must be produced to the FTA within 30 days of request. They need not be filed, but must be ready and available when requested.

What KGRN Provides as a Business Valuation Service Provider in Dubai

UAE-specific valuations are not like typical advisory services. These valuations need to be authorised, understand CTP009 and MD 173, have OECD-compliant transfer pricing methods and the documentation to withstand FTA challenges.

- CTP009-compliant QIP valuations for real estate developers taking advantage of the transition window under MD 120 of 2023

- IAS 40 / MD 173 opening value assessments to support the depreciation election and ongoing annual reporting

- Transfer pricing benchmarking and documentation in line with UAE CT Law and OECD guidelines: Master File, Local File and Related Party Disclosure

- Independent valuations of businesses for mergers and acquisitions, shareholder disputes, fundraising or impairment, always separate from your auditor

- FTA audit services – filing documentation packages, voluntary disclosure, and assisting with reconsideration requests.