The United Arab Emirates is known for its thriving economy, excellent infrastructure, investor-friendly environment and one of the world’s largest oil producing countries. The UAE government decided to diversify its economy and sources of income beyond oil resources and to provide a stable living for their residents.

As part of the major step towards economic diversification, on 23 August 2017, the Federal Tax Authority issued Federal Decree-Law No. 8 of 2017 on Value Added Tax (UAE VAT Law). The members of the Gulf Corporation Council (GCC) introduced VAT across the UAE in January 2018.

Understanding the VAT framework is essential for any businesses to run their operations effectively and get them aligned with Federal Tax Authority (FTA) regulations. Let us explore how VAT applies for businesses and what sectors are subject to VAT, exempt categories, and more

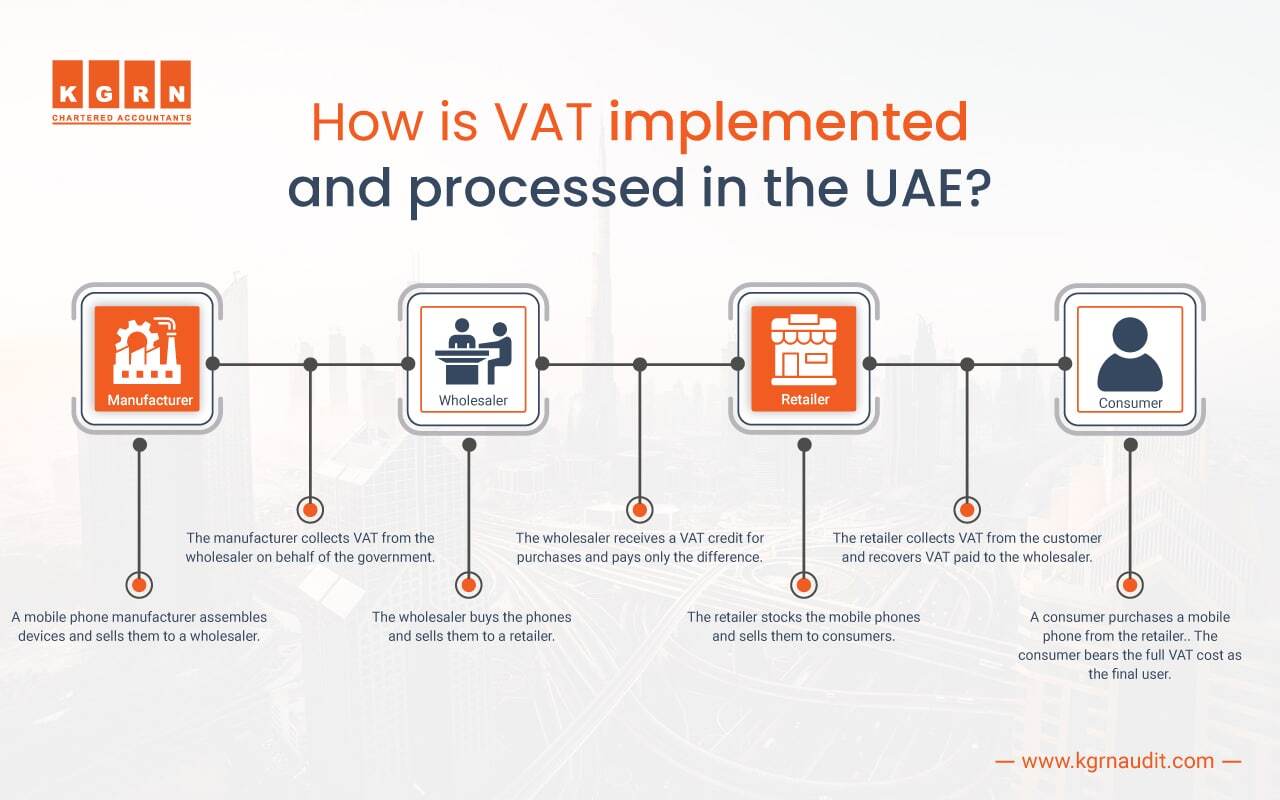

How is VAT implemented and processed in the UAE?

VAT is an indirect tax or general consumption tax that is imposed on goods and services at each stage of the supply chain and is levied by an intermediary on behalf of the government. It is usually levied on the end-consumers while purchasing goods or services.

The standard VAT rate in UAE is 5% which is applicable for most of the goods and services and there are certain exemptions such as zero-rated supplies and exempt supplies. The VAT rate is the lowest when compared with other countries as the VAT law is designed in such a way that it does not majorly impact their consumers. Also, for certain essential goods and services like healthcare, education, the VAT is either zero-rated or exempted. This ensures that the government wants to minimize the burden of consumers while also generating revenue.

| Sales [AED] | VAT Amt Recovered On Purchase [AED] (Input Tax) | VAT Amt [5%] Recovered On Sale [AED] (Output Tax) | Net VAT Payable | |

| Producer | 100 | 5 | 5 | |

| Manufacturer | 200 | 5 | 10 | 5 |

| Retailer | 300 | 10 | 15 | 5 |

| Consumer | Total VAT Paid by End-Consumer – 15 |

How Is VAT Calculated?

Here’s the formula for calculating VAT:

Net VAT Payable = Output VAT – Input VAT

According to the Federal Tax Authority, the Net VAT payable is the value of the supply charged to the customer excluding the VAT charges.

Output VAT: Output VAT or Output Tax is the tax collected by a business on behalf of the government from their customers on the sale of goods and services.

Input VAT: Input VAT or Input Tax is the VAT amount paid for any purchase of goods or services

The VAT amount collected during the sales during the taxable period (Output VAT) and how much Input VAT is recoverable should be determined. By subtracting the VAT on purchases from VAT on sales, the Net VAT payable is calculated. If the input VAT is greater than output VAT, no VAT will be due, and the difference will be refunded.

VAT Categories in UAE

It is important for businesses operating in the UAE as well as the resident to understand the VAT categories.

Standard VAT Rate: The standard 5% VAT rate is applicable for most of the goods and services provided in the UAE.

Zero-Rated Supplies: Some of the export activities and essential products or services sectors such as healthcare, and education are zero-rated. This means that these services are applicable for 0% VAT rate whereas they can still claim input VAT.

Exempt Supplies: Residential property supplies and certain financial services are exempt from VAT. This means that any irrecoverable cost in VAT will not be applied for the purchase of properties. Hence VAT will not be charged and cannot be claimed for these goods and services.

VAT Registration Threshold in UAE

The thresholds for businesses to register for VAT in UAE will be based on their taxable supplies which involves various factors such as standard-rated supplies, exempt supplies, zero-rated supplies, imported goods and reverse charges received.

Mandatory Registration

If the total value of the annual taxable supplies and imports within the UAE exceeds AED 375,000, then it is mandatory for businesses to register for VAT

Voluntary Registration

If the total value of the annual taxable supplies and imports within the UAE exceeds AED 187,000, then businesses can voluntarily register for VAT. Even if the total expenditure of a business exceeds the voluntary registration threshold, they can voluntarily register for VAT.

Non-resident Registration

Non-resident doing business activity in UAE which is categorised as taxable supply under VAT law should register for VAT regardless of the threshold requirement mentioned above.

VAT-related Requirements For businesses

It is significant that all businesses operating in UAE should maintain their financial records and ensure they are accurate. Businesses that meet the VAT registration threshold should register for VAT. Businesses that does not meet the VAT registration threshold should also maintain their financial transactions and keep their records accurate, in case they meet the threshold in future or if there could be any amendment in the threshold.

VAT-registered businesses must:

Charge 5% VAT on any taxable supplies to their customers.

Reclaim the VAT amount paid on purchases that are categorized as taxable supplies.

Maintain records of transactions and proper accounts for the government to verify that they operate in accordance with the rules and regulations.

If you are a business registered for VAT, then you should provide a report on a regular basis, that declares the amount of VAT that you have charged your customers during sales and the amount of VAT you have paid to the government. The report should be formally submitted to the government through the online portal.

If the VAT amount you have charged is more than the VAT you have paid, then the excessive amount should be paid to the government. If the VAT charged is less than you have paid, then the difference amount can be reclaimed.

Zero-rated Supplies under UAE VAT Law

The following categories of supplies are considered as zero-rated supplies under UAE VAT law and charged 0% VAT rate for these services:

- Export of goods and services to places outside the GCC

- International transportation services and related supplies

- Supply that involves sea, air, and land transportation (e.g., ships and aircraft)

- Investment-grade precious metals such as gold and silver with a purity of 99% or more

- First-time supply of newly built residential properties within three years of completion

- Supply of certain education services, along with related goods and services

- Supply of certain healthcare services, along with related goods and services

VAT-Exempt Sectors in UAE

The following activities will be exempt from VAT in UAE:

- The supply of certain financial services

- Residential properties

- Bare land

- Local passenger transport

Partial Exemption For VAT in UAE

A VAT-registered business that can fully recover input taxes if the transactions are related to a taxable supply made or intended to be made. If the expenditure is related to a non-taxable supply (e.g. exempt supply), then the registered taxable person may not recover the input tax paid.

In specific situations, an expense can be both related to taxable and non-taxable supplies, in such cases, the registered person cannot be able to apportion between the taxable and non-taxable supplies. Hence, the businesses should use input tax as a basis for the apportionment in the first instance, and there are some other methods that are fair and approved by the FTA.

VAT for Government Entities

Even the government organizations are generally subject to VAT, as the government wants to establish fair treatment of tax when it comes to the comparison of government and private entities.

Certain supplies made by the government will be excluded from VAT if the particular supply is not competitive to the private sector or the government entity is the sole supplier of such goods and services. To facilitate a level-playing field between outsourced activities and insourced activities, certain governments can claim VAT refunds.

If a taxable supply is provided for the government entities, the treatment of such supplies will be the same as provided for any private customer. As the VAT treatment of supplies is dependent on the nature of the supply and not on the recipient of the supply.

Conclusion

VAT is more than a standard tax – it is a multifaceted system that impacts both businesses and consumers. For businesses, it reflects their pricing mechanism, cash flow management, and accounting methods. A solid understanding of VAT methods and implementation in UAE helps businesses in maintaining financial compliance and planning. It is also essential to stay up-to-date with the latest VAT regulations in UAE and ensure adherence to avoid repercussions.

FAQ

What is the Threshold For VAT in UAE?

Businesses with the total value of annual taxable supplies exceeding AED 375,000, must register for VAT. There is a voluntary registration threshold of AED 187,000.

What is the VAT rate in UAE and how is it calculated?

The standard VAT rate of 5% is applied on most of the goods/services. For example, If a consumer buys a product at the price of AED 1050, with the VAT rate is 5% of AED 1050, then the Input VAT is AED 1050 x 5% = AED 50.

What are the VAT exempt sectors in UAE?

The following are the VAT-exempted sectors in UAE:

- Healthcare (specific services)

- Education (specific services)

- Export of goods and services

- Residential properties (first sale)

- Precious Metals (Specific conditions)

What is the difference between exempt supplies and zero-rated supplies under VAT law in UAE?

The exempt supplies will not be subject to VAT and the input VAT is not claimable. But the zero-rated supplies are subject to 0% VAT and the input VAT is recoverable

What is the reverse charge mechanism in VAT regulations?

Reverse charge mechanism is used to calculate VAT in case of imported goods or services and it helps to streamline the cross-border activities.