In the United Arab Emirates, the UAE Corporate Tax will be applied over the whole country and will apply equally to all business and commercial activity, with the exception of natural resources, which will continue to be taxed at the Emirate level in the UAE.

The following rates will be applied to company tax in the United Arab Emirates:

In addition to being subject to UAE Corporate Tax and being required to register and submit a Corporate Tax report, free zone enterprises will be eligible for Corporate Tax vacations and zero percent taxation as long as they meet all regulatory requirements and do not engage in Corporate Tax activity on the UAE’s inland territory, which is the United Arab Emirates.

According to the press release and FAQs, a new tax rate will be adopted for big multinational firms that fulfill the conditions of the Organization for Economic Cooperation and Development’s ‘Pillar Two’ of the Base Erosion and Profit Shifting project Corporate Tax Rates (i.e. that have consolidated global revenues above EUR 750m).

Except for a few exclusions and revisions, corporate tax will be imposed on the accounting net profit reported in the business’s financial records, not on the gross profit. If you suffer a tax loss after the Corporate Tax Effective Date, you may carry it forward and apply it to your taxable income in subsequent quarters.

In the following cases, there would be no UAE Corporate Tax imposed:

Income from dividends, capital gains, and other investment returns received by foreign investors; employment income, real estate income, savings income, investment returns, and other income generated by individuals acting in their own personal capacity that cannot be traced back to a UAE trade or corporation.

Exemptions from UAE Corporate Tax will be granted for the products listed below:

- Intra-group transfers that qualify; capital gains and dividends on qualified shareholdings that qualify

- Taxation and reorganisation of corporations

Taxation of corporations

Interest, dividends, royalties, and other payments, both local and international, will be unaffected by the change.

Withholding taxes are charged on corporate income in the United Arab Emirates, and international tax credits will be available for taxes collected by UAE enterprises on revenue received outside the country.

Corporate Tax in UAE will be transmitted electronically once every fiscal period, and there will be no necessity to make advance payments based on provisional tax data in the future.

Group firms in the United Arab Emirates may join a tax group and submit a single tax return for the whole group, as well as transmit tax losses to other group members, according to the law.

Regarding transfer pricing regulations and documentation requirements, the UAE Corporate Tax system will follow the Transfer Pricing Guidelines issued by the Organization for Economic Cooperation and Development.

Understanding the UAE Corporate Tax Regime

The introduction of corporate tax in the UAE marked a significant evolution in the country’s fiscal framework. Effective for financial years beginning on or after June 1, 2023, the UAE implemented a federal corporate tax regime under Federal Decree-Law No. 47 of 2022. This system applies to businesses across the country, including those in free zones, but with targeted incentives to preserve the UAE’s attractiveness as a global business hub.

The standard corporate tax rate is 9% on taxable income exceeding AED 375,000, with 0% on income up to that threshold. The primary purpose of this tax is to diversify revenue sources beyond oil, align the UAE with international standards (such as OECD principles), promote transparency, and support sustainable economic growth while maintaining a competitive edge for investors.

For free zone businesses, the regime offers substantial relief. Qualifying Free Zone Persons can benefit from a 0% corporate tax rate on their qualifying income, provided they meet specific conditions. This incentive supports the UAE’s vision of fostering innovation, trade, and foreign investment in designated zones.

Corporate Tax Benefits for UAE Free Zone Businesses

UAE free zones remain highly appealing for entrepreneurs and investors due to several key advantages under the corporate tax framework:

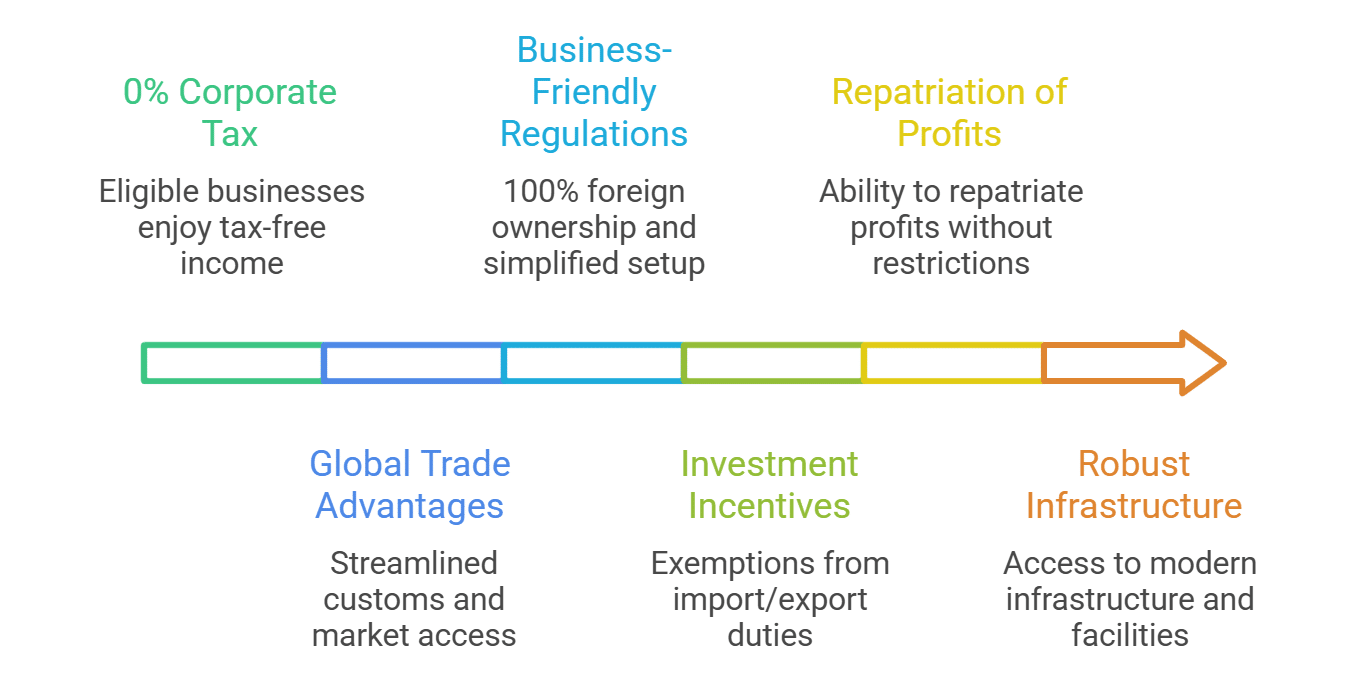

- 0% corporate tax on qualifying income — This is the standout benefit for eligible businesses, allowing significant tax savings on core operations that align with free zone incentives.

- Global trade advantages — Free zones facilitate international business with streamlined customs, logistics, and access to markets, complemented by tax-efficient structures for qualifying activities like trading, manufacturing, and services.

- Business-friendly regulations — Free zones offer 100% foreign ownership in many cases, simplified setup processes, and sector-specific support, making them ideal for SMEs and startups.

- Investment incentives — Beyond tax relief, free zones provide exemptions from import/export duties on qualifying goods, repatriation of profits, and robust infrastructure.

These elements combine to make UAE free zones a strategic choice for foreign investors and company owners seeking efficiency and growth.

What Is a Qualifying Free Zone Person?

A Qualifying Free Zone Person (QFZP) is a juridical entity registered or established in a UAE free zone that satisfies strict criteria to access the 0% corporate tax benefit on qualifying income. Not all free zone companies automatically qualify; they must actively comply.

Key eligibility criteria include:

- Being a Free Zone Person (incorporated, established, or registered in a free zone, including branches of non-residents).

- Maintaining adequate substance in the free zone, such as sufficient staff, assets, operating expenses, and core income-generating activities conducted locally (with proper supervision if outsourced).

- Deriving Qualifying Income from approved activities.

- Complying with the arm’s length principle for transfer pricing and maintaining required documentation.

- Preparing and maintaining audited financial statements.

- Ensuring non-qualifying revenue does not exceed de minimis thresholds (generally 5% of total revenue or AED 5 million, whichever is lower).

- Not electing to be subject to standard corporate tax rules.

Failure to meet any condition results in loss of QFZP status, potentially for the entire tax period or longer.

Income Eligible for 0% Corporate Tax

For a QFZP, qualifying income enjoys the 0% corporate tax rate. This includes income from:

- Qualifying activities such as manufacturing or processing of goods/materials, trading of qualifying commodities, holding shares/securities for investment, ownership/management of ships, reinsurance, fund/wealth management, headquarters/treasury services to related parties, financing/leasing of aircraft, distribution/logistics in designated zones, and certain ancillary activities.

- Transactions with other free zone persons (subject to exclusions).

- Foreign-sourced income derived from qualifying activities.

- Income from qualifying intellectual property (under nexus rules).

Qualifying income must align with the business’s licensed activities and substance requirements.

Income Subject to 9% Corporate Tax

Even for QFZPs, not all income qualifies for the 0% rate. Non-qualifying income is taxed at 9% (above the AED 375,000 threshold):

- Income from transactions with mainland UAE entities (unless part of qualifying distribution/logistics in designated zones).

- Income from excluded activities, such as banking, insurance (non-reinsurance), finance/leasing (non-aircraft/ships), ownership/exploitation of immovable property (except commercial in free zones under conditions), or non-qualifying IP.

- Revenue exceeding de minimis limits for non-qualifying sources, which can taint the entire QFZP status.

Businesses must carefully segregate and allocate expenses to determine taxable portions accurately.

Compliance Requirements for Free Zone Companies

To maintain benefits and avoid penalties, free zone companies must adhere to rigorous compliance standards:

- Maintain proper accounting records in line with IFRS or acceptable standards.

- Prepare audited financial statements (mandatory for QFZPs and often for others based on revenue thresholds).

- Register for corporate tax with the Federal Tax Authority (FTA) and obtain a Tax Registration Number (TRN).

- File corporate tax returns annually, even if no tax is due, within specified deadlines.

- Comply with transfer pricing rules, including documentation to demonstrate arm’s length dealings.

- Ensure adequate substance and monitor de minimis thresholds.

Non-compliance can lead to loss of QFZP status, audits, or penalties.

How KGRN Supports Free Zone Businesses with Corporate Tax Compliance

At KGRN Chartered Accountants, we specialize in guiding free zone businesses through the complexities of UAE corporate tax. Our services include:

- Tax advisory to assess QFZP eligibility and optimize structures.

- Assistance with tax registration and TRN applications.

- Compliance support, including preparation of audited financials, transfer pricing documentation, and return filings.

- Strategic corporate tax planning to maximize qualifying income and minimize exposure to the 9% rate.

Our team of experienced UAE tax advisors ensures clear, practical solutions tailored to your operations.

Common Corporate Tax Mistakes Free Zone Companies Should Avoid

Many free zone businesses encounter pitfalls that jeopardize their tax benefits:

- Misunderstanding qualifying income and incorrectly classifying mainland transactions or excluded activities.

- Failing to maintain adequate substance, such as insufficient local operations or poor outsourcing oversight.

- Keeping inadequate accounting records or delaying audited financial statements.

- Ignoring transfer pricing requirements, leading to non-arm’s length transactions.

- Exceeding de minimis thresholds for non-qualifying revenue without proper monitoring.

- Incorrect tax classification of income sources, resulting in unexpected 9% liability.

Proactive review and professional guidance help avoid these issues.

Conclusion

UAE free zone companies continue to enjoy compelling advantages under the corporate tax regime, particularly the potential for 0% corporate tax on qualifying income as a Qualifying Free Zone Person. This supports global competitiveness, efficient operations, and long-term growth for foreign investors, SMEs, and entrepreneurs.

However, these benefits hinge on strict compliance with eligibility criteria, substance requirements, and ongoing obligations. Navigating the rules effectively requires diligence and expertise.

We recommend consulting professional corporate tax advisors to evaluate your position, ensure compliance, and optimize your tax strategy. At KGRN Chartered Accountants, we are committed to helping free zone businesses thrive in this evolving landscape.

Related posts:

Chapter 10 – Transactions with Related Parties and Connected Persons

Chapter 10 – Transactions with Related Parties and Connected Persons  Chapter Three – Exempt Person Under UAE Corporate Tax Law

Chapter Three – Exempt Person Under UAE Corporate Tax Law  MoF New Decision – Unincorporated Partnerships

MoF New Decision – Unincorporated Partnerships  Corporate Tax Accounting Standards in UAE: A Guide For Businesses

Corporate Tax Accounting Standards in UAE: A Guide For Businesses  Complete Guide to General Interest Deduction Limitation Rule in UAE Corporate Tax

Complete Guide to General Interest Deduction Limitation Rule in UAE Corporate Tax